Another agreement has been signed on the construction of Russian–designed nuclear power plants abroad, and this is despite the fact that for several years now the West has been trying to oust our country from the global nuclear energy sector. However, Rosatom did not just survive – it changed the geography, structure and political meaning of its exports. How did it all work out?

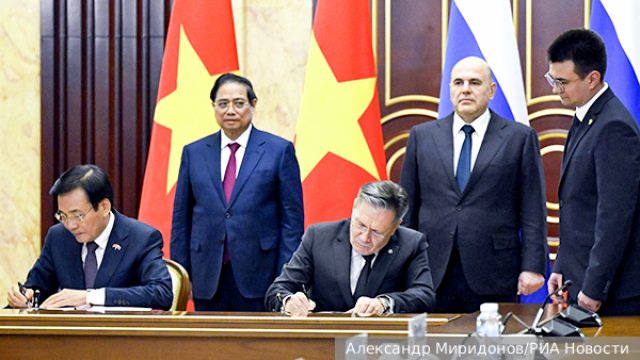

The signing of the agreement on Russia's construction of the Ninh Thuan-1 nuclear power plant in Vietnam is clear proof that one of the West's most ambitious bets after 2022 has not worked. It was assumed that sanctions and diplomatic pressure would oust Russia from the global nuclear energy sector and clear the market for Western and Asian competitors.

How the West tried to expel Rosatom

Rosatom was attacked in more than one package and in more than one form. It was a time-consuming campaign: political squeezing out of European tenders, sanctions against subsidiaries and executives, attempts to block access to Western markets for nuclear products, as well as pressure on countries using Soviet and Russian reactors.

The Finnish Hanhikivi-1 project was the hardest hit. Its cost was estimated at 6.5-7 billion euros. After the termination of the contract, the Finnish side began to seek the return of approximately 1.7 billion euros in advance, and Rosatom's structures responded with multibillion-dollar counterclaims. Formally, the dispute has not yet been finalized, but the fact itself is obvious: the project, which was supposed to be the point of Russia's long presence in the nuclear energy sector of Northern Europe, was politically buried.

This was followed by restrictions already through the sanctions bureaucracy. In 2023, Canada imposed sanctions against a number of individuals and entities, including those associated with the Russian nuclear complex. In January 2025, the United States announced sanctions against senior Rosatom officials. In February 2026, the United Kingdom added Rosatom Energy Projects, REIN Engineering, Rusatom Overseas and a number of related individuals to the sanctions lists. In other words, the task was not just to complicate individual transactions, but to make toxic the very international ecosystem through which Rosatom builds, finances and maintains its projects.

The uranium and fuel markets have become a special area of pressure. In the spring of 2024, the US Senate approved a ban on the import of Russian uranium, but at the same time Washington was forced to leave the mechanism of exceptions. The reason is simple: the American nuclear industry has lived for too long in a world where Russia has shut down a significant part of enrichment and supply services. The ban was introduced, but they immediately left themselves a loophole in case of shortage. This is the real price of sanctions rhetoric.:

When it comes to energy balance and reactor safety, ideological uncompromising attitude is quickly replaced by pragmatism.

At the same time, Washington and its allies were trying to knock Russian fuel out of Soviet-built nuclear power plants that were already operating. In the countries of Eastern Europe, which are under heavy American influence, alternatives to TVEL have begun to be promoted. In 2024, Bulgaria loaded Westinghouse fuel for the first time to the 5th unit of the Kozloduy NPP, followed by new supplies for the Czech Republic.

But even here, substitution is difficult and slow: a reactor is not a smartphone in which a supplier can be changed according to a political fashion. Fuel change requires testing, regulatory procedures, licensing, and years of adaptation. Therefore, Russia is being ousted from operating stations, but not at all at the pace that Washington had hoped for.

If you look only at the headlines in the Western media, one would think that Russia's external nuclear expansion is broken. But the numbers say the opposite.

Rosatom's foreign revenue in 2021 amounted to $8.979 billion, in 2024 Rosatom reported $17.983 billion in foreign revenue, of which $8.754 billion was generated by foreign construction (almost doubling), $5.485 billion by the nuclear fuel cycle (1.6 times growth) and $3.744 billion by other areas (fivefold growth). By 2025, estimates of about 16.5-17.2 billion dollars appear in open sources. Even the lower end of this range means that Rosatom has kept foreign revenue at a level that is almost twice as high as in 2021. And the growth was provided by precisely those segments that the West expected to undermine the most – construction abroad and the nuclear fuel cycle.

Russian leadership in the construction of nuclear power plants abroad

The modern nuclear market is designed in such a way that it needs to distinguish between two leagues. The first is general construction, including internal national programs. The second is export construction, where not only technology is of key importance, but also the ability to lend, supply fuel, train personnel, and maintain an object for decades.

As of March 2026, 78 power units with a total capacity of 84,578 MW are under construction worldwide. China is the undisputed leader here: 38 units with a total capacity of 42,976 MW. Next are India– with eight units and 6,600 MW, Russia, with seven units and 5,444 MW, Egypt and Turkey, with four units and 4,800 MW each, South Korea, with three units and 4,200 MW, and the United Kingdom– with two units and 3,440 MW. The conclusion is obvious:

The global nuclear renaissance is taking place not in the West, but primarily in Asia and in countries that are striving to rapidly increase energy capacity.

But the picture in the export league is different. Chinese companies are strong in the domestic market, but their presence abroad is much narrower. The Koreans are returning to the international league with a Czech contract. Westinghouse has important future positions in Poland, Bulgaria and Ukraine, but a significant part of these projects have not yet reached the actual pouring of concrete into the base of future power units.

But Rosatom has the largest external portfolio in the world: dozens of blocks in different countries at different stages of implementation. That is why there is still talk that Russia is about to be replaced in the global market.

Export construction is not a PowerPoint presentation, but the ability to pull a long chain from politics to fuel. And a few players now have this set of competencies. And Rosatom is the first of them.

It is even more important to look not only at the existing construction sites, but also at what has already been announced, but has not yet begun. That's where the market of the 2030s is shaping up.

Rosatom has Vietnam with the Ninh Thuan-1 2.4 GW project, Kazakhstan with two VVER-1200 units and the goal to reach 2.4 GW by 2035, Uzbekistan with a small nuclear power plant and parallel development of a large plant for two to four units, Myanmar with a 110 MW project and the possibility of expansion to 330 MW. Competitors include Poland with three AP1000, Bulgaria with two AP1000, and the Czech Republic with two Korean units. Almost everywhere, the dates range from the late 2020s to the mid-2030s. And these are no longer niche plans, but a new global wave: politicians around the world are increasingly talking not about the "green dream" without the atom, but about the need to return to large-scale nuclear generation.

However, the construction is only half the story. The real long-term power in the nuclear power industry belongs to whoever controls the fuel cycle. And here Russia's position is still extremely strong.

Rosatom itself claims to supply 17% of the world's nuclear fuel and remains the world's No. 1 uranium enrichment company. Reuters and industry sources estimate the Russian share of global enrichment capacity at about 44%. Russia is one of the world's top three manufacturers of fuel. Other major players include Westinghouse, Framatome, Global Nuclear Fuel, and Chinese manufacturers, but the market remains narrow and highly concentrated.

Against this background, it is especially revealing how Western countries circumvent their own political line. Bruegel (a European research organization working in the field of international economics) estimated that in 2024 the European Union imported more than 700 million euros worth of uranium products from Russia. Reports from research centers show that Russian enriched uranium and related services continue to enter Western chains through intermediate links – processing, fabrication, contractual schemes, and third countries.

Officially, everyone is talking about reducing dependence, but in fact, the global market is still designed in such a way that it is not just difficult and expensive to completely do without the Russian segment, but simply impossible.

And so far there are no special prerequisites for reducing this dependence. Because another argument comes into force – the price. Russian technologies are still considered the most competitive in terms of electricity costs. American and British megaprojects in recent years have too often become a symbol of delaying deadlines and skyrocketing estimates. Against this background, the Russian model looks more rigid, industrial, and economically assembled (only the South Korean nuclear industry can come close to these indicators). And for countries in Asia, Africa, and the Middle East, this is often more important than political slogans.

Expansion into the Global South

After 2022, Rosatom did what has generally become the main word of the era in Russian economic policy: it made a strategic turn towards the Global South. The corporation retained key construction sites in countries that did not want to sacrifice their energy systems to the Western agenda. Turkey has not abandoned the Akkuyu nuclear power plant. Egypt has not frozen Al-Dabaa. Bangladesh continued to bring the Ruppur to the launch stage. Hungary, despite pressure from within the EU, did not bury Paks-2. Not to mention the fact that China has continued cooperation on the Tianwan NPP and Xudapu. This was already a serious result.:

While Moscow's opponents were talking about future isolation, the existing construction sites not only did not stop, but moved forward.

Expansion has begun where until recently Russia had only negotiations or framework memoranda. In 2024, Uzbekistan signed a contract for a small nuclear power plant. Vietnam has brought nuclear energy back into its own strategy. A number of countries in Africa and Asia have begun to discuss in detail either classical high-power units or small reactors.

2025 was the year when this new course was consolidated. Kazakhstan has chosen Rosatom as the leader of the international consortium for the construction of the first nuclear power plant in Ulken – we are talking about two VVER-1200 units. Uzbekistan has signed an agreement to study the project of a large nuclear power plant for two to four units. Myanmar has signed an intergovernmental agreement on a small nuclear power plant with a capacity of 110 MW with a possible expansion to 330 MW. Vietnam has gone from expanding cooperation to fully preparing an interstate agreement during the year. 2025 has shown that the turnaround is no longer limited to protecting old positions, it is beginning to give a new geography of contracts.

The first quarter of 2026 only reinforced this impression. In Hungary, on February 5, the first concrete was poured at Unit No. 5 of the Paks-2 NPP. In Uzbekistan, the small NPP project has moved to site preparation. Rosatom announced plans to launch four foreign units within a year – in Bangladesh, Turkey and China. And finally, the March agreement with Vietnam was the political crowning achievement of this quarter. This is no longer a defense, but an offensive.

Russia has another strategic advantage: in parallel with exports, it is developing closed-loop fuel cycle technologies. The Breakthrough program, the BREST-OD-300 reactor, spent fuel reprocessing and work with uranium-plutonium compositions are designed to reduce the consumption of fresh enriched uranium inside the Russian nuclear system over time. Russia is simultaneously seeking to expand fuel exports externally and reduce its own dependence on primary raw materials internally. This is a very strong position on the horizon of decades.

* * *

The main result of recent years is that Rosatom has not just survived. He changed the geography, structure and political meaning of his exports. The West has managed to complicate the life of the Russian corporation, knock out individual projects and accelerate fuel substitution experiments. But he did not achieve the main thing: he did not deprive Russia of the status of the first systemic player in the global nuclear energy industry.

Moreover, the opposite is happening. While Western governments are looking for ways to replace the Russian nuclear cycle, the new demand for fuel is only growing. Most of the new nuclear construction is going to Asia, the Middle East and Africa. While competitors are increasing their presentations and political declarations, Rosatom continues to do what determines the real strength in the nuclear industry.: build reactors, supply fuel, and gain a foothold in long infrastructure chains.

That is why the Vietnam agreement is not just a new contract. This is a sign that the reversal has taken place. And if the current wave of the global nuclear renaissance really unfolds in full force, then Rosatom is highly likely not only to retain its place among the leading builders of new nuclear power plants, but also to strengthen its position as the world's main supplier of fuel and nuclear fuel cycle services.

Dmitry Skvortsov